FCGグループのニュースレターをお届けします。

FCGグループのニュースレターをお届けします。

2022年06月29日ベトナム

2022年6月税務ニュース

1. 納税延長に関して規定している政令第34/2022/ND-CP号の実施(税務総局から発行された2022年6月23日付のオフィシャルレター第2194/TCT-KK号)

2022年5月税務ニュースにて2022年5月28日に政府が2022年における付加価値税(VAT)及び法人所得税(CIT)、個人所得税(PIT)及び土地レンタル料の納付延長について規定する政令第34/2022/ND-CP号を発行したことをご案内致しましたが、延長申請書の記載方法及び納税者の申告支援ソフトウェア(eTax, iCaNhan, HTTK)、税務当局による納税延長のプロセスについては、税務総局から発行された2022年6月23日付のオフィシャルレター第2194/TCT-KK号をご参照下さい。

2. 証憑書類、インボイスについて規定している政令第123/2020/ND-CP号及び減税、免税について規定している15/2022/ND-CP号の修正(2022年6月20日付の政令第41/2022/ND-CP号)

●発行後誤りが発見された電子インボイスの処理方法(破棄/修正/別インボイス発行)に対する当局の承認または否認の通知書は、政令第123/2020/ND-CP号に添付されていた01/TB-SSDT様式の代わりに01/TB-HDSS様式が適用される。

●付加価値税(VAT)を8%に減税される商品、サービスのインボイス発行に関する規定を以下の通り修正する。

・控除方式を採用する会社の場合、税率が異なる商品やサービスを提供する際に、それぞれの商品やサービスの税率を明記しなければならない(税率が異なる)。なお、現行規定(政令第15/2022/ND-CP号)においては、VAT減税の対象である商品、サービスに対してインボイスを分けて発行しなければならず、別途インボイスを発行しない場合、VAT減税が適用されないものと定められている。

・直接方式を採用する会社の場合、商品やサービスを提供する際に、インボイス上に規定に基づいて減額された金額を明記しなければならない。

本政令(政令第41/2022/ND-CP号)施行前の2022年2月1日から2022年6月20日の期間に本政令に基づいた内容でVATインボイスが発行されていた場合においても、VAT減税は適用されるものとする(発行済インボイスの修正不要、かつ、税務ペナルティも科せられない)。

本政令は、発行日より有効となる。

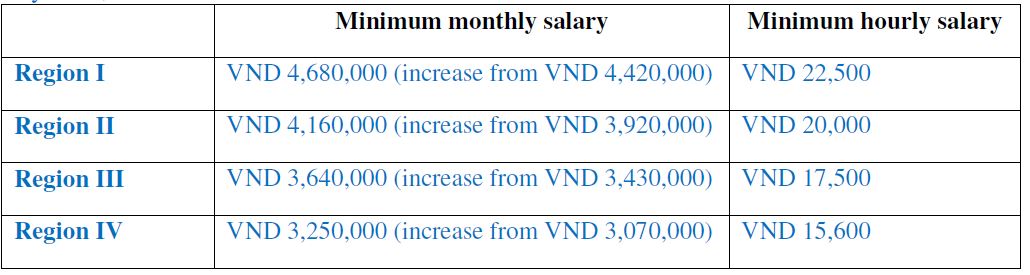

3. 2022年7月1日から最低賃金が6%上昇

ベトナム政府は、2022年6月12日付で労働契約書を締結して就労する労働者に対する最低賃金について規定する政令第38/2022/ND-CP号を発行した。以前の政令と異なり、月額の最低賃金だけでなく、時間単位の最低賃金も規定している。詳細は以下の通りである。

※当政令は7月1日から有効となる。

4. 輸出加工企業からベトナム国内企業への物品貸与(税関総局から発行された2022年4月21日付のオフィシャルレター第1400/TCHQ-TXNK号)

●税関手続きについて

輸出加工企業(EPE)は、自社製品を製造するためにベトナム国内企業に物品を貸与(リース・レンタル)する場合、当該企業は一時輸出の通関手続きを実施し、当該国内企業が一時輸入の通関手続きを実施すること;かつ契約終了時、当該国内企業が一時輸出の通関手続きを実施し、当該EPE企業が貸与した物品に対して再輸入の通関手続きを実施すること

●貸与品に対する輸入税

ベトナム国内企業が契約書に基づいて自社の製造を実施するためにEPE企業から物品の貸与を受ける場合、輸出入税法第107/2016/QH12号第16条9項aに規定されている輸入税の免税を適用することができず、当該企業は一時輸入する際に輸入税を申告・納付しなければならない。また、当該貸与品を再輸出する際は、輸出入税法第107/2016/QH12号第19条1項dに規定されている輸入税の還付も適用できない。貸与品への輸入税の算出は、税務省から発行された通達第60/2019/TT-BTC号第1条9項に従うものとする。

●一時輸入再輸出による貸与品に対するVAT

・国内企業がEPEから貸与を受けた物品に対して、一時輸入として通関申告した場合、該当貸与品はVATの課税対象ではない。貸与期間が満了したが、当該企業が引き続き当該貸与品を使用し、再輸出していない場合、貸与期間が満了した際に直ちにVAT及び政府から発行された2018年4月20日付の政令第59/2018/ND-CP号第1条12項に規定されている輸入税を申告、納付しなければならない。

・使用中に貸与品が故障し、再輸出できずに処分しなければならず、かつ当該企業がすでに現行法律に基づいて処分手続きを実施した場合、これらの物品に対して、当該企業はVATを申告・納付する必要はない。

●追加申告

2019年10月15日(通達第60/2019/TT-BTC号が有効となった日付)以降に申告し、まだ再輸出していない貸与品に対して、当該企業は通関申告ミスと認識しており、財務省から発行された2019年8月30日付の60/2019/TT-BTC 号第1条9項に規定されている追加申告可能なケースに該当すれば、規定に基づき追加申告を実施することができる。

税関当局は、追加申告の条件、金額、税政策及び追加申告関連の規定を確認し、当該ケースを処理するものとする。

●過払した税額の処理

当該企業は、税額を誤申告し、その結果として税額を過払いしたが、追加申告できるケースに該当し、過払した税額は還付される(未払税、遅延利息、罰金がある場合は相殺)。税関当局は追加申告の理由及び申告書、証憑書類等を確認し、税額を確定する。

●一時輸入再輸出の物品を結果として再輸出しない場合の税務処理

・国内企業は、契約書に基づいて自社の製造を実施するためにEPEから物品の貸与を受ける場合、貸与期間満了時に、貸与品を再輸出しなければならない。

・当該企業が貸与品を再輸出しない場合、貸与期間満了後に申告し、規定に基づき税金、罰金を納付しなければならない。貸与期間が満了後、申告・納付内容に不足がある場合は、税関当局が、政府から発行された2020年10月19日付の政令第126/2020/ND-CP号第17条4項に基づき追徴額を確定するものとする。

5. 発注がない故に製造を一時停止した固定資産の減価償却費(バクニン省から発行された2022年5月9日付のオフィシャルレター第1475/CTBNI-TTHT号)

発注がない故に企業が製造を一時停止した未使用の機械について、季節生産による9か月未満の非稼働期間、または12か月未満の修理、移転、定期保守のいずれにも該当しない場合、当該企業は一時停止期間中にも固定資産の償却を実施しなければならない。しかし、一時停止期間中に発生した減価償却費は、企業の事業活動の目的に使用されていないため、損金算入費用として計上できないものとする。

【PDF】Tax bulletin_June 2022_JP (Final)

TAX BULLETIN June 2022

1. General Department of Taxation issued Official letter No. 2194/TCT-KK dated 23rd June 2022 on the implementation of Decree 34/2022/ND-CP on extension of deadline for tax payments

As refer to our Tax Bulletin of May 2022, the Government issued Decree 34/2022/ND-CP on the extension of the deadline for paying VAT, CIT, PIT and land rental in 2022 on 28th May 2022. Please read the Official Letter No. 2194/TCT-KK dated 23rd June 2022 of the General Department of Taxation for instructions on how to declare required information in the Request for extension of tax payment in 2022, tax declaration applications (eTax, iCaNhan, HTKK) and internal process of tax payment extension by tax authorities.

2. Decree No. 41/2022/ND-CP dated 20th June 2022 of the Government amending and supplementing Decree No. 123/2020/ND-CP on invoices and the Decree No. 15/2022/ND-CP providing tax exemption and reduction policies

● Issuing Form No. 01/TB-HDSS – Notice of receipt and processing results of e-invoices with errors to replace Form No. 01/TB-SSDT, Appendix IB enclosed to the Decree No. 123/2020/ND-CP.

● Amending regulations on invoicing for goods and services eligible for VAT reduction to 8% as follows:

– In case a business establishment applies credit method of calculating VAT, when selling goods or providing services with different tax rates, the VAT invoice must clearly state the tax rate of each good or service. According to current regulations, business establishments must issue separate invoices for goods and services eligible for VAT reduction. In case a business establishment does not issue a separate invoices for goods and services eligible for VAT reduction, VAT reduction will be not accepted.

– In case a business establishment applies direct method of calculating VAT, when selling goods or providing services, the sales invoice must clearly state the amount of the reduction as prescribed.

– In case from 1st February to 20th June 2022, those business establishments which has issued VAT invoices according to the above provisions will still be entitled to VAT reduction and will not have to adjust the invoice, and will not be penalized.

This Decree took effect from the date of signing.

3. Minimum salaries increase by 6% from 1st July 2022

On 12 June 2022, the Government issued Decree 38/2022/ND-CP on new minimum salaries which will come into effect from 1 July 2022. Unlike previous Decrees, Decree 38/2022/ND-CP stipulates not only the minimum monthly salaries but also the minimum

hourly ones, as follows:

4. Treatment with respect to goods hired, borrowed from EPEs by domestic enterprises (Official letter No. 1400/TCHQ-TXNK dated 21st April 2022 of General Department of Customs)

● Customs procedures

In case where an EPE leases or lends its goods to a domestic enterprise for production of products of the EPE, the export processing enterprise shall open the declaration of temporary export and the domestic enterprise shall open the declaration of temporary import; upon terminating the lease or lending contract, the domestic enterprise shall perform procedures for re-export of the leased or lent goods, and the EPE shall perform procedures for re-import of these goods.

● Import duty on hired or borrowed goods

In case where a domestic enterprise hires or borrows goods from an EPE under a hiring or borrowing contract to serve its manufacturing, it shall not be eligible for exemption from import duty as provided for in Point a Clause 9 Article 16, Law on Export and Import Duties No. 107/2016/QH12, and it is required to declare and pay import duty when temporarily importing such goods, and shall also not be eligible for refund of the paid import duty when re-exporting such goods as provided for in Point đ Clause 1 Article 19, the Law on Export and Import Duties No. 107/2016/QH13 because these are hired or borrowed goods. The taxable value of hired or borrowed goods shall be determined in accordance with Clause 9 Article 1, Circular No. 60/2019/TT-BTC of the Ministry of Finance.

● VAT on goods hired or borrowed in the form of temporary import for re-export

– Goods hired or borrowed by a domestic enterprise from an EPE and for which the declaration of temporary import has been registered shall not be subject to VAT. Upon the end of the hiring or borrowing period, if the domestic enterprise fails to re-export such hired or borrowed goods, it shall, immediately after ending the hiring or borrowing period, declare and pay VAT and import duty on a new customs declaration as provided for in Clause 12 Article 1, Decree No. 59/2018/ND-CP dated 20th April 2018 of Government.

– In case of the hired or borrowed goods which are damaged while being used and for which destruction procedures have been carried out in accordance with regulations of law, the domestic enterprise is not required to declare and pay VAT on these hired or borrowed goods.

● Additional declaration

If an error in the customs value of an enterprise’s hired or borrowed goods which are declared on the declaration of temporary import registered on 15th October 2019 or afterwards (the effective date of the Circular No. 60/2019/TT-BTC) and have not yet been re-exported is found and the enterprise is entitled to make additional declaration of the taxable value of hired or borrowed goods as prescribed in Clause 9 Article 1, Circular No. 60/2019/TT-BTC dated 30th August 2019 of the Ministry of Finance, the enterprise shall make an additional declaration as provided.

The customs authority shall inspect conditions for making the additional declaration, the additionally declared customs value, tax policies and other regulations on the additional declaration as provided.

● Handling the overpaid tax

If an enterprise is entitled to make an additional declaration due to wrong statement of the taxable value resulting in the tax paid greater than the amount payable, the overpaid amount shall be refunded when the taxpayer no longer has outstanding tax, late payment interest or fine. The customs authority shall inspect the reasons for making additional declaration, the submitted declaration, relevant documents used for determining the customs value and tax policies as provided.

● Handling the tax in case of failure to re-export temporarily imported goods

– If a domestic enterprise hires or borrows goods from an EPE under a hiring or borrowing contract to serve its manufacturing, it shall re-export such hired or borrowed goods upon the expiry of the lease or lending period.

– The enterprise that fails to re-export their hired or borrowed goods shall, immediately after ending the hiring or borrowing period, perform procedures for registration of a new customs declaration and fully pay taxes and fines (if any) as provided. If the enterprise fails to declare and fully pays taxes upon the expiry date of the hiring or borrowing period, the customs authority shall assess the tax amount payable according to Clause 4 Article 17, Decree No. 126/2020/ND-CP dated 19th October 2020 of Government.

5. Depreciation of unused fixed assets due to no orders (Official Letter No. 1475/CTBNI-TTHT dated 9th May 2022 of Bac Ninh Tax Department)

In case of production stoppage due to no purchase orders, which is not due to either seasonal production for an inactive period of less than 9 months, nor repair, relocation, period icmaintenance for a period of less than 12 months, the company still has to depreciate fixed assets during the production stoppage. However, the depreciation expense in such period is not considered deductible expenses as it does not serve business activities.

【PDF】Tax bulletin_June 2022_EN

BẢN TIN THUẾ Tháng 6 năm 2022

1. Tổng cục Thuế ban hành Công văn số 2194/TCT-KK ngày 23/6/2022 về tổ chức triển khai Nghị định 34/2022/NĐ-CP về gia hạn nộp thuế

Như chúng tôi đã đưa tin trong Bản tin thuế Tháng 5 năm 2022, ngày 28/5/2022, Chính phủ đã ban hành Nghị định 34/2022/NĐ-CP gia hạn thời hạn nộp thuế GTGT, thuế TNDN, thuế TNCN và tiền thuê đất trong năm 2022. Các doanh nghiệp có thể tham khảo công văn số 2194/TCT-KK ngày 23/6/2022 của Tổng cục thuế để được hướng dẫn về cách khai thông tin Giấy đề nghị gia hạn năm 2022, các ứng dụng hỗ trợ người nộp thuế kê khai (eTax, iCaNhan, HTKK) và quy trình xử lý gia hạn nộp thuế của cơ quan thuế.

2. Nghị định 41/2022/NĐ-CP ngày 20/6/2022 sửa đổi Nghị định 123/2020/NĐ-CP về hóa đơn, chứng từ và Nghị định 15/2022/NĐ-CP quy định miễn, giảm thuế

● Quy định Mẫu số 01/TB-HĐSS – Thông báo về việc tiếp nhận và kết quả xử lý về việc hóa đơn điện tử đã lập có sai sót thay thế Mẫu số 01/TB-SSĐT Phụ lục IB ban hành kèm theo Nghị định số 123/2020/NĐ-CP.

● Sửa đổi quy định về việc lập hóa đơn đối với hàng hóa, dịch vụ được giảm thuế GTGT xuống 8% như sau:

– Trường hợp cơ sở kinh doanh tính thuế GTGT theo phương pháp khấu trừ thì khi bán hàng hóa, cung cấp dịch vụ áp dụng các mức thuế suất khác nhau thì trên hóa đơn GTGT phải ghi rõ thuế suất của từng hàng hóa, dịch vụ. Theo quy định hiện nay, cơ sở kinh doanh phải lập hóa đơn riêng cho hàng hóa, dịch vụ được giảm thuế GTGT. Trường hợp cơ sở kinh doanh không lập hóa đơn riêng cho hàng hóa, dịch vụ được giảm thuế GTGT thì không được giảm thuế GTGT.

– Trường hợp cơ sở kinh doanh tính thuế GTGT theo phương pháp tỷ lệ % trên doanh thu thì khi bán hàng hóa, cung cấp dịch vụ thì trên hóa đơn bán hàng phải ghi rõ số tiền được giảm theo quy định.

– Trường hợp từ ngày 01/02 đến ngày 20/06/2022, cơ sở kinh doanh đã thực hiện lập hóa đơn GTGT theo quy định trên thì vẫn được giảm thuế GTGT và không phải điều chỉnh lại hóa đơn, không bị xử phạt về thuế và hóa đơn.

Nghị định này có hiệu lực từ ngày ký ban hành.

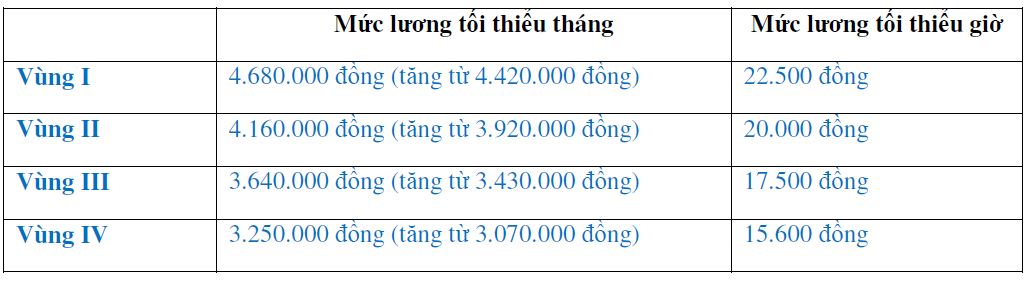

3. Mức lương tối thiểu vùng tăng 6% từ ngày 1/7/2022

Chính phủ ban hành Nghị định 38/2022/NĐ-CP ngày 12/6/2022 quy định mức lương tối thiểu đối với người lao động làm việc theo hợp đồng lao động từ ngày 01/7/2022. Khác với các Nghị định trước đây, Nghị định 38/2022/NĐ-CP không chỉ quy định mức lương tối thiểu theo tháng mà còn quy định mức lương tối thiểu theo giờ, cụ thể như sau:

4. Hướng dẫn xử lý đối với hàng hóa doanh nghiệp nội địa thuê, mượn của DNCX (Công văn số 1400/TCHQ-TXNK ngày 21/4/2022 của Tổng Cục Hải quan)

● Về thủ tục hải quan

Trường hợp doanh nghiệp chế xuất (DNCX) cho doanh nghiệp nội địa thuê, mượn hàng hóa để phục vụ sản xuất ra sản phẩm cho chính doanh nghiệp chế xuất thì DNCX mở tờ khai tạm xuất, doanh nghiệp nội địa mở tờ khai tạm nhập; sau khi kết thúc hợp đồng thuê, mượn, doanh nghiệp nội địa thực hiện thủ tục tái xuất, DNCX thực hiện thủ tục tái nhập lại số hàng hóa đã cho thuê, mượn để sản xuất hàng hóa xuất khẩu này.

● Về thuế nhập khẩu đối với hàng hóa đi thuê, mượn

Trường hợp doanh nghiệp nội địa thuê, mượn hàng hóa của DNCX theo hợp đồng thuê, mượn để phục vụ sản xuất thì doanh nghiệp nội địa không được miễn thuế nhập khẩu theo quy định tại điểm a khoản 9 Điều 16 Luật Thuế xuất khẩu, thuế nhập khẩu số 107/2016/QH12, doanh nghiệp nội địa phải kê khai nộp thuế nhập khẩu khi tạm nhập và không thuộc các trường hợp được hoàn thuế nhập khẩu đã nộp khi tái xuất theo quy định tại điểm đ khoản 1 Điều 19 Luật Thuế xuất khẩu, thuế nhập khẩu số 107/2016/QH13 do là trường hợp đi thuê, mượn. Trị giá tính thuế nhập khẩu đối với hàng hóa đi thuê, mượn thực hiện theo quy định tại khoản 9 Điều 1 Thông tư 60/2019/TT-BTC của Bộ Tài chính.

● Về thuế GTGT đối với hàng hóa đi thuê, mượn theo hình thức tạm nhập-tái xuất

– Đối với số hàng hóa của doanh nghiệp nội địa đi thuê, mượn của DNCX, doanh nghiệp nội địa đã đăng ký tờ khai theo loại hình tạm nhập thì không thuộc đối tượng chịu thuế GTGT. Trường hợp đã hết thời hạn cho thuê, mượn nhưng doanh nghiệp nội địa tiếp tục sử dụng, không tái xuất thì ngay sau khi hết thời hạn thuê, mượn doanh nghiệp nội địa phải kê khai, nộp thuế GTGT cùng với thuế nhập khẩu trên tờ khai hải quan mới theo quy định tại khoản 12 Điều 1 Nghị định số 59/2018/NĐ-CP ngày 20/4/2018 của Chính phủ.

– Trường hợp trong quá trình sử dụng hàng hóa thuê, mượn bị hư hỏng không thể tái xuất, buộc phải tiêu hủy và đã thực hiện thủ tục tiêu hủy theo quy định của pháp luật thì doanh nghiệp nội địa không phải kê khai nộp thuế GTGT đối với số hàng hóa thuê, mượn này.

● Về khai bổ sung

Đối với hàng hóa đi thuê, mượn thuộc các tờ khai tạm nhập đăng ký từ ngày 15/10/2019 (ngày có hiệu lực của Thông tư số 60/2019/TT-BTC) và chưa tái xuất, doanh nghiệp thuê, mượn xác định có sai sót trong việc khai trị giá hải quan và thuộc các trường hợp được phép khai bổ sung tờ khai hải quan theo trị giá tính thuế của hàng đi thuê, mượn quy định tại khoản 9 Điều 1 Thông tư 60/2019/TT-BTC ngày 30/8/2019 của Bộ Tài chính nêu trên thì thực hiện khai bổ sung theo quy định.

Cơ quan hải quan thực hiện kiểm tra các điều kiện để được khai bổ sung, trị giá hải quan khai bổ sung, chính sách thuế và các quy định về khai bổ sung để xử lý theo quy định.

● Về xử lý số tiền thuế nộp thừa

Trường hợp doanh nghiệp thuộc trường hợp được khai bổ sung do khai sai về trị giá tính thuế dẫn đến số tiền thuế đã nộp lớn hơn số tiền thuế phải nộp thì được hoàn trả số tiền thuế nộp thừa khi người nộp thuế không còn nợ tiền thuế, tiền chậm nộp, tiền phạt. Cơ quan hải

quan thực hiện kiểm tra lý do khai bổ sung, tờ khai hải quan, các chứng từ, tài liệu có liên quan để xác định trị giá hải quan và chính sách thuế theo đúng quy định.

● Về xử lý thuế đối với trường hợp không tái xuất hàng hóa nhập khẩu theo hình thức tạm nhập – tái xuất

– Trường hợp doanh nghiệp nội địa thuê, mượn hàng hóa của DNCX theo hợp đồng thuê, mượn để phục vụ sản xuất thì sau khi kết thúc thời hạn thuê, mượn, Công ty phải thực hiện tái xuất số hàng hóa đã thuê, mượn.

– Trường hợp doanh nghiệp không thực hiện tái xuất số hàng hóa đã thuê, mượn thì ngay sau khi kết thúc thời hạn thuê, mượn phải đăng ký tờ khai hải quan mới, nộp đủ tiền thuế, tiền phạt (nếu có) theo quy định. Trường hợp không kê khai nộp đủ các loại thuế khi đã kết thúc thời hạn đi thuê, mượn thì cơ quan hải quan thực hiện ấn định thuế theo quy định tại khoản 4 Điều 17 Nghị định số 126/2020/NĐ- CP ngày 19/10/2020 của Chính phủ.

5. Chi phí khấu hao TSCĐ trong thời gian dừng sản xuất do không có đơn hàng (Công văn số 1475/CTBNI-TTHT ngày 09/05/2022 của Cục Thuế tỉnh Bắc Ninh)

Trường hợp công ty không có đơn hàng phải dừng sản xuất, máy móc không sử dụng không thuộc trường hợp phải tạm dừng do sản xuất do mùa vụ với thời gian dưới 09 tháng, tạm thời dừng để sữa chữa, để di rời di chuyển địa điểm, để bảo trì, bảo dưỡng theo định kỳ với thời gian dưới 12 tháng thì Công ty vẫn phải trích khấu hao TSCĐ trong thời gian dừng sản xuất.

Tuy nhiên, khoản chi phí khấu hao TSCĐ trong thời gian tạm dừng đó không được tính vào chi phí được trừ khi xác định thu thập chịu thuế TNDN do không phục vụ sản xuất kinh doanh.

【PDF】Tax bulletin_June 2022_VN

〈お問い合わせ先〉

Fair Consulting Vietnam Joint Stock Company

|

Hanoi Office 3F, Leadvisors Place,41A Ly Thai To St Hoan Kiem Dist., Hanoi Vietnam Tel:+84-24-3974-4839 石井 大輔 日本国公認会計士 |

Ho Chi Minh Office Room 902, 9th Floor, HD Tower 25 Bis Nguyen Thi Minh Khai St, Ben Nghe Ward, District 1, Ho Chi Minh City, Vietnam Tel:+84-28-3910-1480 藤原 裕美 オーストラリア国公認会計士 Email: hi.fujiwara@faircongrpcom.jpn.org 草野 航平 |