FCGグループのニュースレターをお届けします。

FCGグループのニュースレターをお届けします。

2022年05月30日ベトナム

2022年5月税務ニュース

1. 2022年における納税延長

2022年5月28日、政府が2022年における付加価値税(VAT)及び法人所得税(CIT)、個人所得税(PIT)、土地レンタル料の納付延長について規定する政令第34/2022/ND-CP号を発行した。主な内容は、以下の通りである。

●適用対象

政令第52/2021/ND-CP号第2条に規定されている全ての納税者に対して、2021年のVAT、CITPIT及び土地レンタル料の納付延長の適用を提案した。

●延長期間

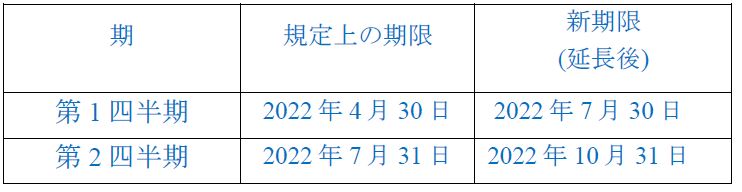

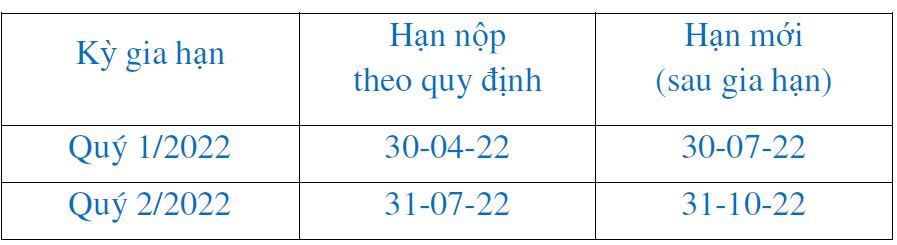

・VAT:

・CIT予定納税:2022年第1四半期、第2四半期予定納税の3か月延長

・2022年に発生する個人事業主のVAT、CIT:2022年12月30日まで延長

・2022年に発生する土地レンタル料:納付金額の50%を対象に6ヶ月延長(2022年5月31日から2022年11月30日となる)。

本政令は、2022年5月28日から2022年12月31日まで有効となる。

2. 預金利息に対する法人所得税の優遇税制(ハイフォン市税務当局から発行された2022年3月22日付のオフィシャルレター第709/CTHPH-TTHT号)

法人所得税の優遇税制が適用されている法人が、資金を金融機関の預金口座に預ける場合、該当金融機関の所在地が優遇地域とそうでない地域とは関係なく、発生した利息は優遇税制の適用対象にならない。当該会社は、優遇税制が適用される生産活動、経営活動と適用されない経営活動に対して、別々に申告、納税しなければならない。また、優遇税制が適用されない利息は、通達第78/2014/TT-BTC号第7条7項に規定される原則に従い、優遇対象でない支払利息とのみ相殺が可能である。

3. 労働契約書終了時の従業員報酬に対する個人所得税(ホーチミン市税務当局から発行された2022年3月21日付のオフィシャルレター第2211/CTTPHCM-TTHT号)

当該会社は、労働契約書終了時に個人所得税の課税対象となる従業員への未払給与、賞与、手当を支給する場合、支給日に基づき下記の通り取り扱うものとする。

●支払日付が労働契約書終了時点前である場合、課税所得に上記の支給額を加算して、累進税率にて個人所得税を計算する。

●支払日付が労働契約書終了時点以降であり、従業員がすでに退職している場合、VND 2,000,000 /回を超過する支給額に対して、税率10%で源泉徴収し支給するものとする。

4. 裾野産業の製品製造プロジェクトに対する法人所得税の優遇税制(バクニン省税務当局から発行された2022年4月7日付のオフィシャルレター第1094/CTBNI-TTHT号)

SPICA ELASTIC VIETNAM CO., LTDは、裾野産業優先製品一覧に属する製品の製造プロジェクトを保有している。当該プロジェクトは2015年1月1日以前に実施し、税法第71/2014/QH13号に規定されている裾野産業製品製造プロジェクトの条件をすべて満たし、かつ2022年3月10日に工商省から優先製品認可書第1201/GXN-BCT号が交付された。当該会社には、以下の通り法人所得税(CIT)の優遇税制が適用される。

●裾野産業製品製造プロジェクトを保有しているが、当該プロジェクトからの収入に対して優遇税制が適用されていない場合、所轄機関より優先製品認可書が交付された課税期間から、裾野産業製品製造プロジェクト向けの優遇税制(優遇税率及び免税期間、減税期間を含む)を適用することができる。

●裾野産業製品製造プロジェクトを保有しているが、当該プロジェクトからの収入が別の優遇税制(裾野産業製品製造プロジェクト向けの優遇税制以外)の適用を受けている、或いは過去に適用を受けていた場合、所轄機関から優先製品認可書が交付された課税期間から、残りの期間に対して、裾野産業製品製造プロジェクト向けの優遇税制(優遇税率及び免税期間、減税期間を含む)を適用することができる。

【PDF版】Tax bulletin_May 2022_JP revise 20220609

TAX BULLETIN May 2022

1. Extension of deadline for tax payments in 2022

On 28th May 2022, the Government issued the Decree No. 34/2022/NĐ-CP the deadline for payment of VAT, CIT, PIT, land rental in 2022 with main contents as follows:

● Taxpayers entitled to tax payment deferral:

The extension will be given to all the same taxpayer specified in Article 2 Decree No.52/2021/ND-CP on the extension the deadline for payment of VAT, CIT, PIT and land rental in 2021.

● Extension period:

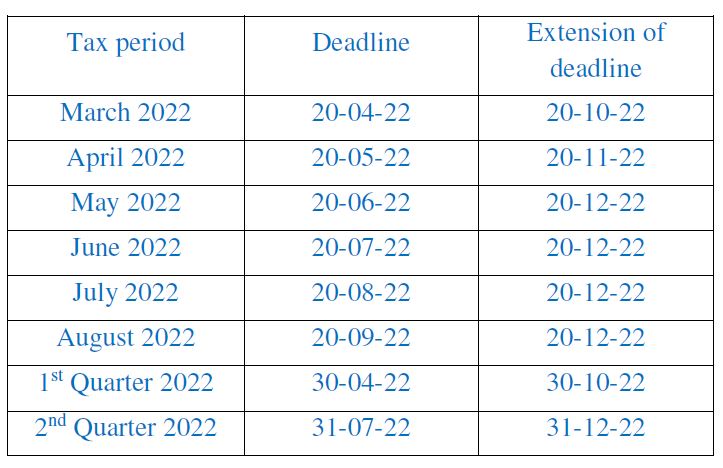

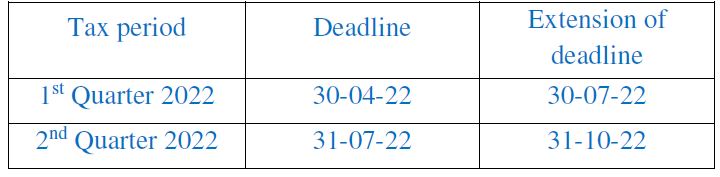

・ VAT payment:

・CIT provisional payment: Deadline for CIT payment in the 1st and 2nd quarters of 2022 will be extended for 3 months

・VAT and PIT payable by business households and individuals in 2022 will extended until 30 December 2022

・Land rental payable in 2022: 06 months of extension for 50% payable amount (from 31 May 2022 to 30 November 2022).

The Decree takes effect from 28th May to 31st December 2022.

2. CIT incentive for interest income from bank deposit (Official Letter No.709/CTHPH-TTHT dated 21st March 2022 of Hai Phong Tax Department)

If the company being entitled to CIT incentives has saving account at a credit institution, regardless of whether the credit institution is inside or outside of the preferential location and incurs interest income paid by the credit institution, this income is not entitled to CIT incentives. For CIT declaration and payment, the company must separately determine income from production and business activities entitled to CIT incentives and income from business activities not entitled to tax incentives. Accordingly, the interest income (not entitled to tax incentives) shall only be offset against interest expenses of non-incentive activities as per principles specified in Clause 7, Article 7, Circular No. 78/2014/TT-BTC.

3. PIT withholding for remuneration payments upon the termination of labour contracts (Official Letter No. 2211/CTTPHCM-TTHT dated 21st March 2022 of Hochiminh City Tax Department)

When terminating the labour contract and company makes final payment for the unpaid monthly salary, bonuses and benefits that are subject to PIT, the PIT withholding will be based on the payment date:

● If the payment date is before the termination date of labour contract, those income shall be treated as taxable income for PIT declaration with progressive tax rate.

● If the payment date is after the termination date of labour contract and the employee has stopped working at the company, for each payment of VND 02 million/payment or more, the company shall withhold PIT at the rate of 10%.

4. CIT incentives for investment projects in the manufacture of supporting industry products (Official No. 1094/CTBNI-TTHT dated 7th April 2022 of Bac Ninh Tax Department)

In case where the SPICA ELASTIC VIETNAM Co., Ltd. has investment projects (new and expanding investment project) in the manufacture of products under the List of prioritized supporting industry products before 1st January 2015 which meet conditions for a project in the manufacture of supporting industry products as provided by the Law No. 71/2014/QH13 and have been granted the Incentive Certificate of manufacturing supporting products No.1201/GXN-BCT dated 10th March 2022 by Ministry of Industry and Trade, CIT incentives will be given in accordance with the following principles:

● If income derived by the Company from the project for manufacturing supporting products has not yet been given CIT incentives, CIT incentives for projects for manufacturing supporting products (including incentive CIT rate and the duration of CIT exemption or

reduction) would have been applied from the tax period when the Incentive Certificate of manufacturing supporting products was granted by the competent authority;

● If income derived by the Company from the project for manufacturing supporting products has been given CIT incentives, other than CIT incentives for projects on manufacturing supporting products, for projects for manufacturing supporting products (including incentive CIT rate and the duration of CIT exemption or reduction) would have been applied for the remaining period as from the tax period when the Incentive Certificate of manufacturing supporting products was granted by the competent authority.

【PDF】Tax bulletin_May 2022_EN_

BẢN TIN THUẾ Tháng 5 năm 2022

1. Gia hạn nộp thuế năm 2022

Ngày 28/5/2022, Chính phủ đã ban hành Nghị định 34/2022/NĐ-CP gia hạn thời hạn nộp thuế GTGT, thuế TNDN, thuế TNCN và tiền thuê đất trong năm 2022 với một số nội dung chính sau:

● Đối tượng gia hạn

Đối tượng gia hạn là toàn bộ đối tượng như được quy định tại Điều 2 Nghị định số 52/2021/NĐ-CP về việc gia hạn thời hạn nộp thuế GTGT, thuế TNDN, thuế TNCN và tiền thuê đất trong năm 2021.

● Thời gian thực hiện gia hạn

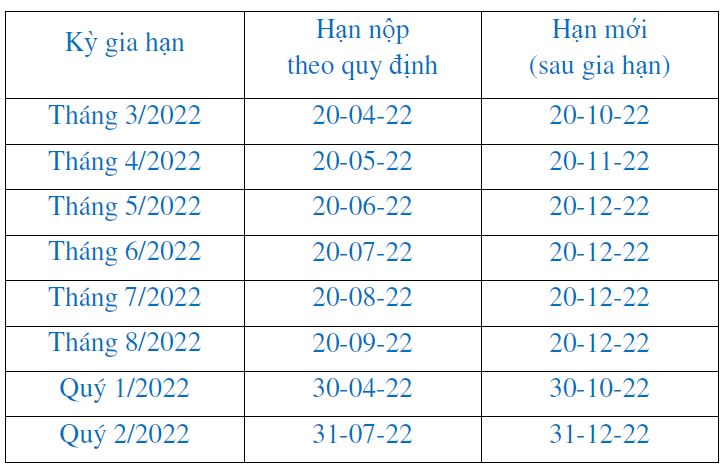

・ Thuế GTGT:

・Thuế TNDN tạm nộp quý I và quý II năm 2022: gia hạn 03 tháng

・Thuế GTGT, thuế TNCN của hộ kinh doanh, cá nhân kinh doanh phát sinh phải nộp của năm 2022: gia hạn chậm nhất đến 30/12/2022

・Tiền thuê đất phát sinh phải nộp năm 2022: gia hạn 06 tháng đối với 50% số tiền phát sinh phải nộp (từ 31/05/2022 đến 30/11/2022).

Nghị định này có hiệu lực từ ngày 28/5/2022 đến hết ngày 31/12/2022.

2. Hướng dẫn về ưu đãi thuế TNDN đối với lãi tiền gửi (Công văn số 709/CTHPHTTHT ngày 22/03/2022 của Cục Thuế TP. Hải Phòng)

Trường hợp công ty đang được hưởng ưu đãi thuế TNDN có khoản tiền nhàn rỗi mang đi gửi tổ chức tín dụng, không phân biệt tổ chức tín dụng ở trong hay ngoài địa bàn ưu đãi và phát sinh khoản lãi tiền gửi do tổ chức tín dụng chi trả thì khoản thu nhập này không được hưởng ưu đãi thuế TNDN. Công ty phải tính riêng thu nhập từ hoạt động sản xuất, kinh doanh được hưởng ưu đãi thuế TNDN và thu nhập từ hoạt động kinh doanh không được hưởng ưu đãi thuế để kê khai, nộp thuế riêng. Theo đó, khoản lãi tiền gửi không được ưu đãi chỉ được bù trừ với chi phí lãi vay phát sinh từ hoạt động không được ưu đãi theo nguyên tắc quy định tại Khoản 7, Điều 7, Thông tư số 78/2014/TT-BTC.

3. Thuế TNCN đối với các khoản thu nhập chi trả cho nhân viên khi chấm dứt hợp đồng lao động (Công văn số 2211/CTTPHCM-TTHT ngày 21/03/2022 của Cục Thuế TP. Hồ Chí Minh)

Trường hợp công ty chi trả khoản tiền lương tháng cuối chưa thanh toán, tiền thưởng, tiền trợ cấp thuộc diện chịu thuế TNCN cho nhân viên khi chấm dứt hợp đồng lao động, Công ty thực hiện khấu trừ thuế dựa trên thời điểm chi trả, cụ thể như sau:

● Nếu thời điểm chi trả trước thời điểm chấm dứt hợp đồng lao động thì công ty cộng các khoản chi vào thu nhập chịu thuế TNCN để tính thuế TNCN theo biểu lũy tiến.

● Nếu thời điểm chi trả sau thời điểm chấm dứt hợp đồng lao động và người lao động đã nghỉ việc, khoản chi tiền từ 2 triệu đồng/lần trở lên thì Công ty khấu trừ thuế theo mức 10%.

4. Hướng dẫn ưu đãi thuế TNDN đối với dự án sản xuất sản phẩm công nghiệp hỗ trợ (Công văn số 1094/CTBNI-TTHT ngày 7/4/2022 của Cục thuế Tỉnh Bắc Ninh)

Trường hợp Công ty TNHH SPICA ELASTIC VIETNAM có dự án đầu tư (đầu tư mới và đầu tư mở rộng) sản xuất sản phẩm thuộc Danh mục sản phẩm công nghiệp hỗ trợ ưu tiên phát triển, thực hiện trước ngày 1/1/2015, đáp ứng đủ các điều kiện của dự án sản xuất sản phẩm công nghiệp hỗ trợ theo qui định của Luật số 71/2014/QH13 được Bộ Công Thương cấp Giấy xác nhận ưu đãi sản xuất sản phẩm hỗ trợ 1201/GXN-BCT ngày 10/3/2022 thì được hưởng ưu đãi thuế TNDN theo nguyên tắc như sau:

● Nếu Công ty có dự án sản xuất sản phẩm công nghiệp hỗ trợ mà thu nhập từ dự án này chưa được hưởng ưu đãi thuế TNDN thì được hưởng ưu đãi thuế TNDN theo điều kiện dự án sản xuất sản phẩm công nghiệp hỗ trợ (bao gồm thuế suất ưu đãi và thời gian miễn,giảm thuế) kể từ kỳ tính thuế cơ quan có thẩm quyền cấp Giấy xác nhận ưu đãi sản xuất sản phẩm hỗ trợ;

● Nếu Công ty có dự án sản xuất sản phẩm công nghiệp hỗ trợ mà thu nhập từ dự án này đã được hưởng hết hoặc đang được hưởng ưu đãi thuế TNDN theo điều kiện ưu đãi khác (ngoài điều kiện ưu đãi đối với dự án sản xuất sản phẩm công nghiệp hỗ trợ) thì được hưởng ưu đãi thuế TNDN theo điều kiện dự án sản xuất sản phẩm công nghiệp hỗ trợ (bao gồm thuế suất ưu đãi và thời gian miễn, giảm thuế) cho thời gian còn lại kể từ kỳ tính thuế kể cơ quan có thẩm quyền cấp Giấy xác nhận ưu đãi sản xuất sản phẩm hỗ trợ.

【PDF】Tax bulletin_May 2022_VN_

〈お問い合わせ先〉

Fair Consulting Vietnam Joint Stock Company

|

Hanoi Office 3F, Leadvisors Place,41A Ly Thai To St Hoan Kiem Dist., Hanoi Vietnam Tel:+84-24-3974-4839 石井 大輔 日本国公認会計士 |

Ho Chi Minh Office Room 902, 9th Floor, HD Tower 25 Bis Nguyen Thi Minh Khai St, Ben Nghe Ward, District 1, Ho Chi Minh City, Vietnam Tel:+84-28-3910-1480 藤原 裕美 オーストラリア国公認会計士 Email: hi.fujiwara@faircongrpcom.jpn.org 草野 航平 |